")

Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

Another great month for Volkswagen Group.

Some 240,000 plugin vehicles were registered in Europe in February, rising 17% year over year (YoY), which is a particularly positive sign when considering that the overall market was down 3% in February, to fewer than one million units.

Interestingly, BEVs are the ones pushing the market upwards, growing 26% YoY in February to 167,000 units. But even more striking is the fact that these positive numbers are being achieved despite Tesla’s current sales crash. The US company saw its deliveries fall by 43% in February.

If we were to exclude Tesla’s volumes from the BEV tally, then BEVs would have surged by 45% in February and 49% YTD!

And with Tesla’s sales crash expected to be eased in Q2, with the volume release of the refreshed Model Y, expect the BEV resurgence to continue, at least until the end of the first half of the year.

Talking about PHEVs, there is also good news here, as they seem ready to leave negative numbers soon. Their YTD numbers were down by only 2%, to 150,000 units.

As such, February saw the plugin vehicle share of the overall European auto market stay at 25% (17% full electrics/BEVs), in line with the year-to-date numbers.

These results also kept the 2025 BEV/PHEV share breakdown at 69% vs. 31%, which is good news for pure electrics, as the final result in 2024 was 67% for BEVs and 33% for PHEVs.

Finally, looking at the sales breakdown between the remaining powertrains, besides the usual steep fall of diesel sales, down 28% YoY to 9% share now (vs. 12% share in February 2024), petrol is now also in a death spiral. Petrol vehicles saw their sales fall by 24% YoY, and their share dropped from 36% a year ago to 28%.

Besides BEVs, the other major winner this year is plugless hybrids, with HEV sales jumping 35% YoY, to 35% share. That’s a significant increase over the 29% HEVs had 12 months ago. This means that 60% of all car sales in Europe in February had some kind of electrification.

With these numbers in mind, one can say that diesel sales should effectively be dead in about three years time, while petrol should share the same fate a few years later (2031? 2032?), which will mean that by 2032, the whole European market will be at least partially electrified.

The 2035 EU target is set to be only zero emission vehicles — i.e., only BEVs (FCEVs and synthetic fuels will remain a small niche). Will the market be ready for it? What do you think? Please leave your comments on this topic. I am looking forward to hearing your feedback on this.

But let’s get back to February’s sales. Looking at the best sellers in several size categories, there is a stark contrast with what is happening in China. Whereas there plugins are showing up and taking over the podiums in each size category, in Europe, the advances have been far less significant. Last year, the only segment where EVs were relevant was the midsize one, and only thanks to Tesla.

In the remaining segments, plugins remain far below the podium level. While prospects for growth are good, the European market is still some three years behind China when it comes to EV adoption and the subsequent merging of the EV market with the mainstream one.

Comparing the European plugin top 10 with the overall top 10 in February, there is still a disconnect. In the overall market, 6 of the top 10 models came from the B-segment (subcompacts), with the remaining coming from the C-segment (compacts).

On the plugin table, only two models (the Renault 5 & Citroen e-C3 EV) came from the B-segment, with compacts having five representatives.

On the flip side, in the plugin top 10, there are three midsize (D-segment) models, while on the overall best sellers table, there are no D-segment representatives….

Plugins are still skewed towards the most expensive models. The EV market needs more affordable models to reach higher volumes if we want to see Europe follow in China’s steps.

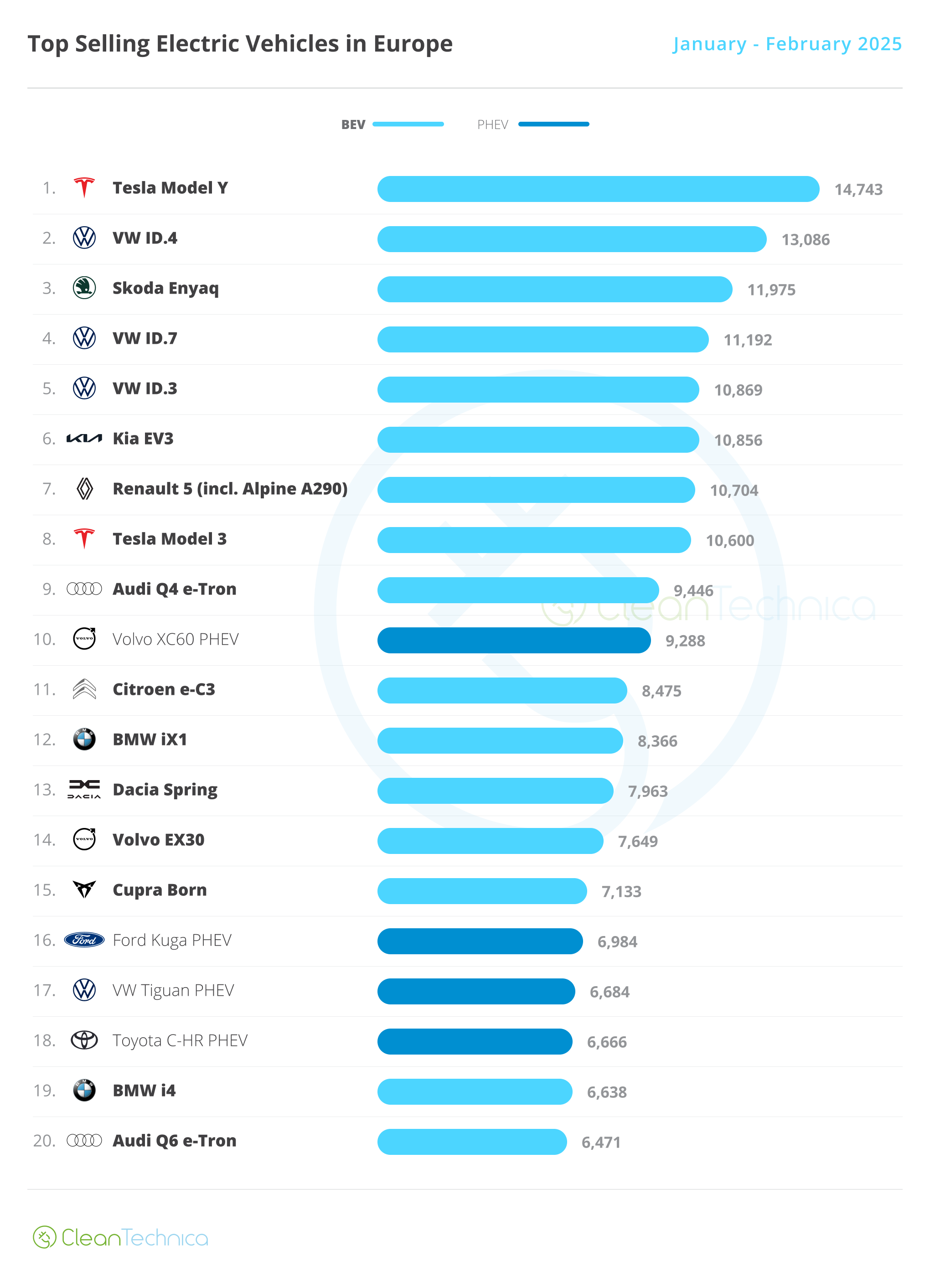

Regarding just EVs, the highlights this month were Tesla back in 1st and 2nd place and the Renault 5 winning its first podium presence. Here’s a more detailed analysis on the top 5 EVs this month:

#1 Tesla Model Y — After losing the January title, Tesla’s crossover was back again in the winning business, thanks to 8,855 registrations. Still, when we compare with the same month last year, deliveries were down by an astounding 56% YoY, or less than half of the sales of February 2024. Remember when I mentioned that 2023/24 would be considered the “peak Model Y” period in Europe? Tesla’s midsizer has hit the market’s natural limits. Sure, the refreshed Model Y version will help things along in March, and especially in Q2, bringing with it a second youth, but do not expect the Model Y’s performance to go above of what it once was. From now on, expect the leader of the European EV market to stay on top in the foreseeable future, but with smaller winning margins and the occasional loss, especially in the first months of each quarter.

#2 Tesla Model 3 — The China-made (but with a US passport) sedan is slowing down, scoring 6,872 registrations in February. That represented a 13% drop YoY. The explanations for this slowdown amount to three things: First are the China tariffs, which have somewhat hurt the sedan’s performance. (The reason why Tesla hasn’t started to make it in Germany is beyond me. Does anyone knows why this hasn’t happened?) The second reason has to do with increased competition, especially the VW ID.7, which has experienced an exponential surge in sales this year, ending February in 7th and maybe giving the Model 3 a run for its money in the 2025 race. Thirdly, Musk’s political shenanigans have started to take a toll on European buyers. For now, this isn’t very significant. I would say it affects just 5% of Tesla’s total sales, meaning that it might affect those who were on the fence between buying a Tesla or another brand as well as those who are more politically motivated. Still, we are only two months into the new US presidency, so who knows where we will be five months from now?

#3 Renault 5/Alpine A290 — Renault’s new star player delivered 6,199 units (with the help of its sportier Alpine twin), a near-record result for the French model and its first podium presence — which will surely be the first of many…. And it’s a good omen for the upcoming Renault 4, which is just starting to get its first demonstration units delivered. While the Renault 5 isn’t class-leading when it comes to interior space and it has too many command stalks, it more than compensates for that in character, be it regarding the eye-catching design or the fun-loving driving dynamics. Together with correct prices and range, those things make it a very compelling offer for European buyers. One can even say that it is a car developed and built for the European mindset.

#4 VW ID.4 — The compact crossover won another top 5 presence in February, with the MEB platform model scoring 6,048 deliveries, meaning 144% growth YoY. This allowed Volkswagen Group to place two models on the best sellers table (as the VW ID.3 took the 5th spot). With improved specs and lower prices (and the small detail that Volkswagen Group needs to sell more BEVs to keep up with the EU’s CO2 rules…), the German crossover is experiencing a second youth. While not the EV enthusiast’s choice, the ID.4 has enough going for it to attract a wide audience. It’s as if Volkswagen Group made the MEB crossovers like ice cream — the VW ID.4 is vanilla ice cream, it is familiar to everyone’s tastes and gets the job done; the Skoda Enyaq/Elroq are the healthy options, for those who value all the taste but low carbs/prices; the Audi Q4 is for those with more expensive tastes who don’t mind paying more in order to have the best chocolate out there; while the Cupra Tavascan is for risk takers, offering a kind of spicy chocolate that most won’t appreciate but a select few will love.

#5 VW ID.3 — Volkswagen’s hatchback has returned to form, scoring 5,435 registrations in February, more than doubling its sales YoY and scoring its best performance of the last eight months. One has to recognize the hard task that the ID.3 inherited when it landed. Filling the VW Golf’s shoes in the EV market was always going to be a daunting task, especially in the context of falling hatchback sales compared to crossovers. Still, the ID.3 has been doing alright lately, being the leader in the compact hatchback category. Considering the current market dynamics, this is all we can ask from it.

Looking at the rest of the February table, a few models deserve a mention, like the record result of the recently introduced #6 Citroen e-C3 EV, 5,407 units, and the continued good results of Volkswagen’s new ID.7, 5,341 registrations, allowing it to end the month in 7th.

Another record performer was the #14 Toyota C-HR PHEV, which scored 3,585 registrations. That was its second record result in a row and allowed the funky crossover to become a serious candidate for the Best Selling PHEV award. Toyota is rising….

Elsewhere, the BYD Seal U (euro-spec BYD Song) has managed another table presence, #20, thanks to 2,912 registrations. This could be a winning formula for Chinese makes in the future, especially considering that plugin hybrids are not affected by tariffs and Chinese OEMs have plenty of them in their domestic lineups.

An interesting fact about this top 20 is that there are five models that weren’t present 12 months ago (Citroen e-C3 EV, Renault 5, Kia EV3, Audi Q6 e-tron, and Toyota C-HR PHEV). So, although the European market is not as feverish with new vehicles as China’s EV market, it is unfair to say that nothing happens.

Below the top 20, outside Volkswagen Group there isn’t much to say, with the exception being the ramp-up of the new Hyundai Inster, which had 2,034 deliveries in February.

As for the German OEM, not happy having eight representatives in the top 20, below the best sellers table, it also has other EVs on the way up, like the case of the Cupra Tavascan (2,434 units, 3rd record in a row) and the production ramp-up of the Skoda Elroq (1,490 units in February). The new Czech crossover could be a sort of secret weapon for the OEM this year, as it might replicate the success of the slightly larger, but also more expensive, Skoda Enyaq.

Heck, even the VW ID. BUZZ helped along, with a record 2,028 units in February, helping to cement VW’s leadership in Europe.

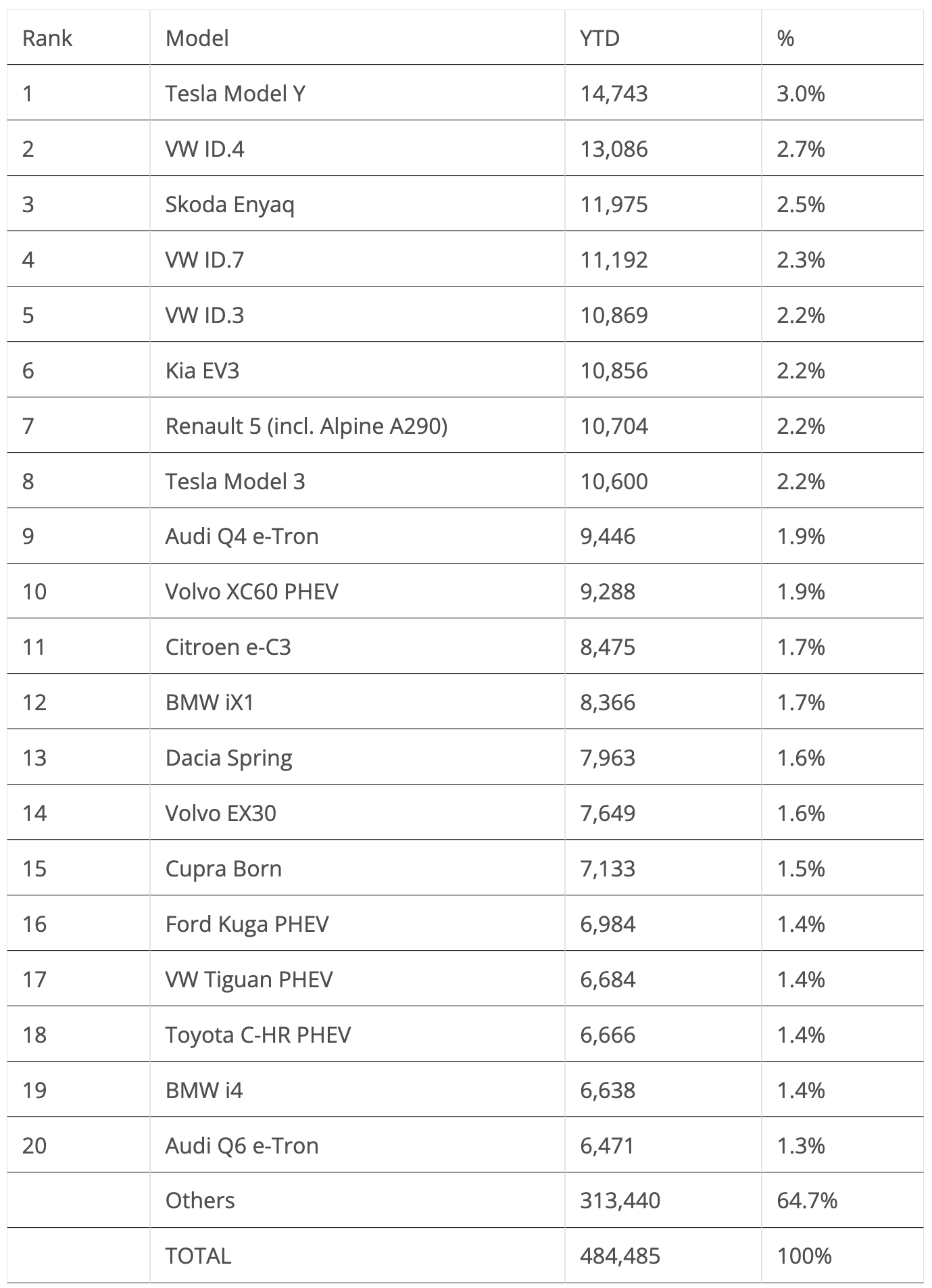

Looking at the 2025 ranking, the big news is the return of the Tesla Model Y to the leadership position, displacing the VW ID.4 to the runner-up position. Still, this year the US crossover should not take for granted the best seller title, which would be its 4th in a row. Not only is the competition selling more than in the past, but above all, the Model Y doesn’t seem able to run at the same pace as it did in past years.

So, while the US crossover is the favorite to win the 2025 title, it won’t be a walk in the park like in previous years.

Below the podium, the highlights were the Tesla Model 3 jumping five positions, into 8th. With the US sedan expected to have a delivery peak in March, one wonders how many more positions it will rise to then. Will it be second? Third? This will serve as an indication as to where the Model 3 might end the year.

Interestingly, ever since it landed in Europe in 2019, the Model 3 has never been below the 2nd spot. Will 2025 be its first year winning bronze?

The other highlights were the rise of the French arch rivals, the Renault 5 and Citroen e-C3 EV, with the former jumping three positions to 7th while the latter surged nine spots to 11th. How high will these two end up? I am still sticking to my guns and saying that the Renault EV could reach 100,000 units this year, which could place it in orbit for a podium position. As for the Stellantis EV, things are more complicated, because it will have strong internal competition, so its demand could be affected by the fact that buyers will have more models to choose from. With this in mind, while a top 10 position seems like a given, it could be hard for it to break into Europe’s top 5.

In the second half of the table, we have two newcomers, of the plugin hybrid variety, with the VW Tiguan PHEV joining the table in 17th and the Toyota C-HR PHEV replacing its stablemate BZ4X as the Toyota representative in the top 20 by ending February in 18th.

Looking at the overall February brand ranking, the fastest growing make in the top 30 was #26 BYD, surging an amazing 211% YoY to a still small 7,000 units. On the opposite side, #21 Tesla was down by 43% YoY, to 16,000 units. So … the King is dead, long live the King?

Not so fast. While it is true that the dynamics between both brands are shockingly opposed, it will take time for BYD to reach Tesla’s sales levels. Having said that, with the current market dynamics, I wouldn’t be surprised if BYD surpassed the US brand in Europe around 2027….

As for the plugin auto brand ranking, Tesla recovered from a horrible January and is now 5th (5.3% in February vs. 4.1% in January), but it is too far behind #1 Volkswagen (11.2%, up 0.1% in February) and #2 BMW (9.5%, down from 9.9% in January) to have ambition of returning to the leadership this quarter. Or even this year.

With Volkswagen this far and this strong, it is hard not so see the German make winning this year’s manufacturer title, effectively ending a three-year Tesla reign in Europe.

Even the 2nd spot could be hard to attain, depending on how currently fluid geopolitics could affect Tesla.

In 3rd we have Mercedes (7.3%, down 0.3% from January), running ahead of #4 Volvo (6.3%, down from 6.4% in January). The three-pointed-star brand is hoping the upcoming CLA sedan could become a strong seller, giving the German brand a star player that its current lineup lacks.

Below the top 5, Renault (4.2%, up 0.2%) is starting to show up on the radar, having risen to 8th, only below #7 Kia (4.8%) and #6 Audi (5%).

Arranging things by automotive group, Volkswagen Group is firmly in the lead, with 26.6% share (up from 19.5% a year ago), a market share that is now comparable to BYD in China and Tesla in the USA?

BMW Group (11.3%, down from 11.5% in January) remained in the runner-up position in February, while #3 Stellantis seems to have stopped the sales bleed (10.1% in February vs. 9.5% in January) thanks to volume deliveries of the Citroen e-C3 EV.

The problem for Stellantis is that just one model being sold in large volumes won’t be enough to keep a podium position, just ask Tesla. With the #2 and #3 best selling EVs scoring fewer than 2,500 units each (Peugeot e-208 EV — 2,427 units; Peugeot e-3008 EV — 2,001 units) in February, they will need to ramp up production of their lower priced models (Fiat Grande Panda EV, Opel Frontera EV, Citroen e-C3 Aircross EV…) sooner rather than later.

Hyundai–Kia (8.4%) surpassed Geely (8.3%, down 0.3%) and is now 4th, with the Koreans betting on their new models (Hyundai Inster, Kia EV4) to gain ground on the Chinese OEM during the coming months.

With the lonely Renault pulling deadweights (Nissan and Mitsubishi) on its back, do not expect the #7 Renault–Nissan Alliance (7%) to disturb the top 5, with the same being said about #6 Mercedes (7.2%) now that Smart has gone to Geely.

Whether you have solar power or not, please complete our latest solar power survey.

Chip in a few dollars a month to help support independent cleantech coverage that helps to accelerate the cleantech revolution!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy